library¶

This module has vocation to concentrate all the functions mentioned in input data files.

Todo

Equations’ indexes are to be improved again.

Note

Contact us as soon as you see something wrong and/or, ambiguous, which is likely given the very early stage of development we are in. Moreover, methods that rely on the structure of their arguments will sooner or later be turned structure-independent.

-

class

iamax.library.ArraysDealer¶ Mixin class that aggregates a bunch of private methods related to (numpy) arrays processing.

-

static

_take(ary: np.ndarray, idx: int, axis: int = 0, keepdims: bool = False)¶ Partialized version of

numpy.takewithmode='clip'to prevent negative indexing and/orIndexError.- Parameters

ary (numpy.ndarray) – Array to be sliced.

idx (int) – Integer index of interest along axis

axis.axis (int) – Axis the slice must be taken along.

0by default.keepdims (bool) – Whether the reduced axis is left in the result as size-one dimension. To

Falseby default.

Note

The original

numpy.takefunction does not feature the keepdims argument, which this method does because of the API divergence on that matter between JAX and NumPy.- Example

>>> ary = np.arange(6).reshape(3, 2) >>> ary array([[0, 1], [2, 3], [4, 5]]) >>> ArraysDealer._take(ary=ary, idx=0) array([0, 1]) >>> ArraysDealer._take(ary=ary, idx=-1) array([0, 1]) >>> ArraysDealer._take(ary=ary, idx=2) array([4, 5]) >>> ArraysDealer._take(ary=ary, idx=3) array([4, 5]) >>> ArraysDealer._take(ary=ary, idx=3, keepdims=True) array([[4, 5]])

-

static

_split(ary: np.ndarray, indices: list[int], axis: int = 0)¶ Split an array into multiple sub-arrays as views into

ary.- Parameters

Note

Compared to its

numpy.split()counterpart, this method can be identity.- Example

>>> ArraysDealer._split(ary=np.arange(3), indices=[1, -1]) [array([0]), array([1]), array([2])] >>> ArraysDealer._split(ary=np.arange(3), indices=[1, None]) [array([0]), array([1, 2]), array([], dtype=int32)] >>> ArraysDealer._split(ary=np.arange(3), indices=[0, -1]) [array([], dtype=int32), array([0, 1]), array([2])] >>> ArraysDealer._split(ary=np.arange(3), indices=[0, 2]) [array([], dtype=int32), array([0, 1]), array([2])] >>> ArraysDealer._split(ary=np.arange(3), indices=[0, None]) [array([], dtype=int32), array([0, 1, 2]), array([], dtype=int32)]

-

static

_infs_to_num(x: np.ndarray, posinf: float = _posinf, neginf: float = _neginf)¶ Replace infinity with numbers.

- Parameters

x (numpy.ndarray) – Array to be processed.

posinf (float) – Value to be used to fill positive infinity values. Set to

numpy.finfo(float).maxby default.neginf (float) – Value to be used to fill negative infinity values. Set to

numpy.finfo(float).minby default.

- Example

>>> ArraysDealer._infs_to_num( ... x=np.array([np.inf, -np.inf, np.nan]), ... posinf=1, neginf=-1 ... ) array([ 1., -1., nan])

-

classmethod

_sum(cls, a: np.ndarray, axis: int = None, keepdims: bool = False)¶ Pro-differentiation NAN-immunized sum of array elements over a given axis.

- Parameters

ary (numpy.ndarray) – Array to be processed.

axis (int) – Axis or axes along which a sum is performed. To

Noneby default.keepdims (bool) – Whether the reduced axis is left in the result as size-one dimension. To

Falseby default.

Note

This (class) method requires a clipping upper bound to prevent floating-point overflow during computations. When summing large values, intermediate results can exceed the maximum representable value for

numpy.float64. Additionally, in the context of second-order derivatives (Hessian), quadratic growth amplifies these values, further increasing the risk of overflow. Clipping ensures numerical stability by constraining intermediate results to a manageable range while preserving the overall summation behavior.

-

static

_divide(n: np.ndarray, d: np.ndarray, nan: float|np.ndarray = 0.0, num_infs: bool = False)¶ Pro-differentiation NAN-immunized divider.

- Parameters

n (numpy.ndarray) – Numerator operand.

d (numpy.ndarray) – Denominator operand.

nan (float or numpy.ndarray) – Value to be used to fill

float('nan')values. Set to0.by default.num_infs (boolean) – Whether positive and negative infinity are to replaced with large finite numbers. Set to

Falseby default.

- Example

>>> ArraysDealer._divide( ... n=(n := np.ones(3)), ... d=np.zeros_like(n), ... ) array([0., 0., 0.])

-

static

_multiply(a: np.ndarray, b: np.ndarray)¶ Pro-differentiation NAN-immunized to-0 multiplicator.

- Parameters

a (numpy.ndarray) – Potentially equal-to-0 operand.

b (numpy.ndarray) – Potentially equal-to-0 other operand.

- Example

>>> a, b = 0, float('inf') >>> a * b nan >>> ArraysDealer._multiply(a, b) array(0.)

Note

Implying this method may not be sufficient if. e.g one of the operands potentially consists in a by-0-division.

-

classmethod

_rdistance(cls, f: np.ndarray, c: np.ndarray)¶ Quasi-scale-invariant division-by-0-immunized symmetrical signed distance computer.

(161)¶\[D(\boldsymbol{f}, \boldsymbol{c}) = \left( \frac{ \boldsymbol{f}-\boldsymbol{c} }{ \sqrt{ \varepsilon^{2} + \boldsymbol{f}^{2} + \boldsymbol{c}^{2} } } \right)\]See also

- Parameters

f (numpy.ndarray) – First array to be processed.

c (numpy.ndarray) – Second array to be processed.

- Example

>>> ArraysDealer._rdistance(f=np.array(2), c=np.array(3)) 0.27732343367971996 >>> ArraysDealer._rdistance(f=np.array(3), c=np.array(2)) -0.27732343367971996 >>> ArraysDealer._rdistance(f=np.array(2), c=np.array(0)) -0.9996876464081226 >>> ArraysDealer._rdistance(f=np.array(0), c=np.array(2)) 0.9996876464081226 >>> ArraysDealer._rdistance(f=np.ones(3), c=np.arange(3)) array([-1. , 0. , 0.45])

-

classmethod

_constancy(cls, ary: np.ndarray, axis: int = None, keepdims: bool = False, where: np.ndarray[bool]|bool = True)¶ Compute a dimensionless smooth subgradient-based manhattan “constancy” metric along a specified axis.

- Parameters

ary (numpy.ndarray) – Array to be processed.

axis (int) – Axis the process must be performed along.

Noneby default.keepdims (bool) – Whether the reduced axis is left in the result as size-one dimension. To

Falseby default.where (numpy.ndarray or bol) – Elements to include in the sum. Set to

Trueby default, which boils down to include all elements.

- Example

>>> a = np.array([[-1., .0, 1.]]) >>> ArraysDealer._constancy(ary=a, keepdims=True) array([[0.82]])

>>> v = np.stack((a, np.ones_like(a), np.zeros_like(a))) >>> ArraysDealer._constancy(ary=v, axis=2, keepdims=True) array([[[0.82]], [[0. ]], [[0. ]]])

-

classmethod

_power(cls, x1: np.ndarray, x2: np.ndarray, num_infs: bool = False, div_by_0_to_0: bool = True, compute_croots: bool = False)¶ Pro-differentiation NAN-immunized power operator.

- Parameters

x1 (numpy.ndarray) – Bases of exponentiation.

x2 (numpy.ndarray) – Exponents.

num_infs (boolean) – Whether positive and negative infinity are to replaced with large finite numbers. Set to

Falseby default.div_by_0_to_0 (bool) – Whether divisions by

0should result in0s instead of resulting innumpy.inf. Set toTrueby default.compute_croots (bool) – Whether complex roots are allowed. Set to

Falseby default.

Attention

Argument

compute_crootsisn’t well tested. Do not use unless you know exactly what you are doing.- Example

>>> ꚙ = np.inf >>> x1 = np.array([ ... 1, .5, .5, 2, 2, -.5, -.5, -2, -2, -2, 0, 0, ꚙ, ꚙ, ꚙ, -ꚙ, ... ]) >>> x2 = np.array([ ... ꚙ, -ꚙ, ꚙ, -ꚙ, ꚙ, -ꚙ, ꚙ, -ꚙ, ꚙ, -.5, ꚙ, -ꚙ, ꚙ, -ꚙ, 0, 0, ... ]) >>> np.vstack(( ... x1, x2, ... ArraysDealer._power( ... x1, x2, num_infs=False, div_by_0_to_0=False, ... ), ... )).T array([[ 1. , inf, 1. ], [ 0.5, -inf, inf], [ 0.5, inf, 0. ], [ 2. , -inf, 0. ], [ 2. , inf, inf], [-0.5, -inf, inf], [-0.5, inf, 0. ], [-2. , -inf, 0. ], [-2. , inf, inf], [-2. , -0.5, 0. ], [ 0. , inf, 0. ], [ 0. , -inf, inf], [ inf, inf, inf], [ inf, -inf, 0. ], [ inf, 0. , 1. ], [-inf, 0. , 1. ]]) >>> np.vstack(( ... x1, x2, ... ArraysDealer._power( ... x1, x2, num_infs=False, div_by_0_to_0=False, ... compute_croots=True ... ), ... )).T array([[ 1. +0.j, inf+0.j, 1. +0.j], [ 0.5+0.j, -inf+0.j, inf+0.j], [ 0.5+0.j, inf+0.j, 0. +0.j], [ 2. +0.j, -inf+0.j, 0. +0.j], [ 2. +0.j, inf+0.j, inf+0.j], [-0.5+0.j, -inf+0.j, inf+0.j], [-0.5+0.j, inf+0.j, 0. +0.j], [-2. +0.j, -inf+0.j, 0. +0.j], [-2. +0.j, inf+0.j, inf+0.j], [-2. +0.j, -0.5+0.j, -2. +0.j], [ 0. +0.j, inf+0.j, 0. +0.j], [ 0. +0.j, -inf+0.j, inf+0.j], [ inf+0.j, inf+0.j, inf+0.j], [ inf+0.j, -inf+0.j, 0. +0.j], [ inf+0.j, 0. +0.j, 1. +0.j], [-inf+0.j, 0. +0.j, 1. +0.j]])

-

classmethod

_weighter(cls, a: np.ndarray, axis: int = -1, keepdims: bool = False)¶ s/e.

- Parameters

ary (numpy.ndarray) – Array to be processed.

axis (int) – Axis or axes along which a sum is performed. To

Noneby default.keepdims (bool) – Whether the reduced axis is left in the result as size-one dimension. To

Falseby default.

-

static

_lminusr_computer(a: np.ndarray, keepdims: bool, axis: int = -1)¶ Compute the difference between the sum of the first (left) half and the sum of the second (right) half along the specified axis.

- Parameters

a (numpy.ndarray) – Array of even horizontal size.

keepdims (bool) – Whether the output has the same number of dimensions as the input.

axis (int) – Axis or axes along which a sum is performed. Set to

-1bu default.

- Example

>>> (a := np.array([[1, 2, 3, 4], [3, 4, 1, 2]])) array([[1, 2, 3, 4], [3, 4, 1, 2]]) >>> ArraysDealer._lminusr_computer(a, keepdims=True) array([[-4], [ 4]])

Another example showing that the first half is favored in case of uneven split.

>>> (a := np.array([[1, 1, 2, 3, 4], [0, 3, 4, 1, 2]])) array([[1, 1, 2, 3, 4], [0, 3, 4, 1, 2]]) >>> ArraysDealer._lminusr_computer(a, keepdims=True) array([[-3], [ 4]])

-

static

-

class

iamax.library.RatesDealer¶ Mixin class that aggregates a bunch of private methods related to rates calculations, conversions, etc.

-

static

_markup_to_margin_rater(mkr: np.ndarray|float)¶ Markup-to-margin rate converter.

\[\text{mgr} = \frac{\text{mkr}}{1 + \text{mkr}}\]- Parameters

mkr (numpy.ndarray or float) – Markup rate to be processed.

- Example

>>> RatesDealer._markup_to_margin_rater(mkr=1.0).item() 0.5

-

static

_margin_to_markup_rater(mgr: np.ndarray|float)¶ Margin-to-markup rate converter.

\[\text{mkr} = \frac{\text{mgr}}{1 - \text{mgr}}\]- Parameters

mgr (numpy.ndarray or float) – Margin rate to be processed.

- Example

>>> RatesDealer._margin_to_markup_rater(mgr=.5).item() 1.0

-

static

-

class

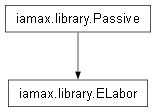

iamax.library.Passive(*_, **__)¶ Class to be (used directly or) inherited from to explicit the idea of an entity not actively at work and whose e.g. consumption/production is determined by the system’s set of constraints.

-

class

iamax.library.AddedOPCosts¶ Class whose name is rather, say, self-explanatory.

-

static

operating_cost_computer(*, operating_costs: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(162)¶\[\v_{q,j} = \sum_{k \in \mcI_j} \v_{q,k}\]with \(\mcI_j\) the index set required to get \(q_j\).

- Parameters

operating_costs (numpy.ndarray) – \((\bv_{q,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

operating_costs’s slice.- Example

>>> a = np.array([[1., 0., 4.]]) >>> AddedOPCosts.operating_cost_computer( ... operating_costs=a ... ) array([[5.]])

Let’s vectorize the above example.

>>> AddedOPCosts.operating_cost_computer( ... operating_costs=np.stack((a, .1*a)) ... ) array([[[5. ]], [[0.5]]])

-

static

-

class

iamax.library.AddedVolumes¶ Class whose name is rather, say, self-explanatory.

-

static

employed_volume_computer(*, employed_volumes: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(163)¶\[q_j = \sum_{k \in \mcI_j} q_k\]with \(\mcI_j\) the index set required to get \(q_j\).

- Parameters

employed_volumes (numpy.ndarray) – \((\bq_k)_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

employed_volumes’s slice.- Example

>>> a = np.array([[1., 0., 4.]]) >>> AddedVolumes.employed_volume_computer( ... employed_volumes=a ... ) array([[5.]])

Let’s vectorize the above example.

>>> AddedVolumes.employed_volume_computer( ... employed_volumes=np.stack((a, .1*a)) ... ) array([[[5. ]], [[0.5]]])

-

static

available_volume_rooter(*, t: int, available_volumes: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero, denoted as

(164)¶\[-1 + \frac{\hq_j}{\sum_{k \in \mcI_j} \hq_k} \approx 0\]with \(\mcI_j\) the index set required to get \(\hq_j\).

- Parameters

t (int) – Year-targeting integer index. Cf.

t, i.e. a_ilocalizations’s integer element.available_volumes (numpy.ndarray) – The \(j\)th \(|\mcL| \times (1 + |\mcI_j|)\)

available_volumes’s slice.

See also

\(|\mcL|\)’s archetype

_ilocalizations.Important

The variable

tis involved to provide the current method with (column-bound) time series arguments. Indeed, the first element of such arguments is always associated with the variable that is being targeted.Note

This method is vectorization friendly over the

-3th axis, if any.- Example

>>> a = np.array([ ... [[0, 0, 0]], ... [[5, 3, 2]], ... [[6, 3, 0]], ... [[3, 6, 0]], ... ]) >>> AddedVolumes.available_volume_rooter( ... t=1, available_volumes=a ... ) array([[0.]]) >>> AddedVolumes.available_volume_rooter( ... t=2, available_volumes=a ... ) array([[-0.45]]) >>> AddedVolumes.available_volume_rooter( ... t=3, available_volumes=a ... ) array([[0.45]])

Let’s vectorize the above example, keeping in mind that the temporal axis must remain first (hence the

numpy.ndarray.swapaxesbelow).>>> (v := np.stack((a, .1*a)).swapaxes(1, 0)) array([[[[0. , 0. , 0. ]], [[0. , 0. , 0. ]]], [[[5. , 3. , 2. ]], [[0.5, 0.3, 0.2]]], [[[6. , 3. , 0. ]], [[0.6, 0.3, 0. ]]], [[[3. , 6. , 0. ]], [[0.3, 0.6, 0. ]]]]) >>> AddedVolumes.available_volume_rooter( ... t=1, available_volumes=v ... ) array([[[0.]], [[0.]]]) >>> AddedVolumes.available_volume_rooter( ... t=2, available_volumes=v ... ) array([[[-0.45]], [[-0.45]]]) >>> AddedVolumes.available_volume_rooter( ... t=3, available_volumes=v ... ) array([[[0.45]], [[0.45]]])

-

static

-

class

iamax.library.ImplicitTransitories¶ Class that abstracts the idea of economic agents who are just accounting artifacts that need, at some point, to be formalized explicitly regarding their “custom QOIs” only.

-

static

transitory_computer(transitories: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(165)¶\[\mcr_j = \sum_{k \in \mcI_j} \mcr_k\]with \(\mcI_j\) the index set required to get \(\mcr_j\).

- Parameters

transitories (numpy.ndarray) – The \(j\)th \(1 \times |\mcI_j|\) slice of

transitories.- Example

>>> a = np.array([[4., 6.]]) >>> ImplicitTransitories.transitory_computer( ... transitories=a ... ) array([[10.]])

Let’s vectorize the above example for free.

>>> ImplicitTransitories.transitory_computer( ... transitories=np.vstack((a, .1*a)) ... ) array([[10.], [ 1.]])

-

static

-

class

iamax.library.ImplicitIncome¶ Class that abstracts the idea of economic agents who are just accounting artifacts that need, at some point, to be formalized explicitly regarding their disposable income only.

-

static

budget_constraint_computer(budget_constraints: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(166)¶\[\mcr_j = \sum_{k \in \mcI_j} \mcr_k\]with \(\mcI_j\) the index set required to get \(\mcr_j\).

- Parameters

budget_constraints (numpy.ndarray) – \((\bmcr_k)_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

budget_constraints’s slice.- Example

>>> a = np.array([[4., 6.]]) >>> ImplicitIncome.budget_constraint_computer( ... budget_constraints=a ... ) array([[10.]])

Let’s vectorize the above example for free.

>>> ImplicitIncome.budget_constraint_computer( ... budget_constraints=np.vstack((a, .1*a)) ... ) array([[10.], [ 1.]])

-

static

-

class

iamax.library.ImplicitEntity¶

Class that abstracts the idea of economic agents who are just accounting artifacts that need, at some point, to be formalized explicitly.

Note

This class has not vocation to be vectorization friendly since implicit entities are recursively function of each others.

-

static

other_costs_computer(other_costs: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(167)¶\[v_{\ootau,\ j} = \sum_{k \in \mcI_j} v_{\ootau,\ k}\]with \(\mcI_j\) the index set required to get \(\mcr_j\).

- Parameters

other_costs (numpy.ndarray) – \((\bv_{\ootau,\ k})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

other_costs.

-

static

net_surplus_computer(net_surplus: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(168)¶\[\pi_{j} = \sum_{k \in \mcI_j} \pi_{k}\]with \(\mcI_j\) the index set required to get \(\mcr_j\).

- Parameters

net_surplus (numpy.ndarray) – \((\bpi_{k})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

net_surplus.

-

static

gross_income_throughput_computer(gross_incomes_throughputs: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(169)¶\[\mcr_{\text{cum},\ j} = \sum_{k \in \mcI_j} \mcr_{\text{cum},\ k}\]with \(\mcI_j\) the index set required to get \(\mcr_j\).

- Parameters

gross_incomes_throughputs (numpy.ndarray) – \((\bmcr_k)_{\text{cum},\ k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

gross_incomes_throughputs.

-

static

input_values_computer(input_values: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(170)¶\[\bmcV_{:,j} = \sum_{k \in \mcI_j} \bmcV_{:,k}\]with \(\mcI_j\) the index set required to get \(\bmcV_{:,j}\).

- Parameters

input_values (numpy.ndarray) – \((\bmcV_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

input_values’s slice.

See also

\(\mcI\)’s archetype

_iidentifiers.- Example

>>> a = np.hstack(( ... _1s := np.ones((4,))[:, None], ... _1s.cumsum(axis=0), .5*_1s, ... )) >>> a array([[1. , 1. , 0.5], [1. , 2. , 0.5], [1. , 3. , 0.5], [1. , 4. , 0.5]]) >>> ImplicitEntity.input_values_computer(input_values=a) array([[2.5], [3.5], [4.5], [5.5]])

Let’s vectorize the above example.

>>> (v := np.stack((a, .1*a))) array([[[1. , 1. , 0.5 ], [1. , 2. , 0.5 ], [1. , 3. , 0.5 ], [1. , 4. , 0.5 ]], [[0.1 , 0.1 , 0.05], [0.1 , 0.2 , 0.05], [0.1 , 0.3 , 0.05], [0.1 , 0.4 , 0.05]]]) >>> ImplicitEntity.input_values_computer(input_values=v) array([[[2.5 ], [3.5 ], [4.5 ], [5.5 ]], [[0.25], [0.35], [0.45], [0.55]]])

-

static

specific_margins_computer(specific_margins: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(171)¶\[\bV^{(\utau)}_{:,j} = \sum_{k \in \mcI_j} \bV^{(\utau)}_{:,k}\]with \(\mcI_j\) the index set required to get \(\bV^{(\utau)}_{:,j}\).

- Parameters

specific_margins (numpy.ndarray) – \((\bV^{(\utau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

specific_margins’s slice.

-

static

trade_margins_computer(trade_margins: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(172)¶\[\bV^{(\jtau)}_{:,j} = \sum_{k \in \mcI_j} \bV^{(\jtau)}_{:,k}\]with \(\mcI_j\) the index set required to get \(\bV^{(\jtau)}_{:,j}\).

- Parameters

trade_margins (numpy.ndarray) – \((\bV^{(\jtau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

trade_margins’s slice.

-

static

sales_taxes_computer(sales_taxes: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(173)¶\[\bV^{(\htau)}_{:,j} = \sum_{k \in \mcI_j} \bV^{(\htau)}_{:,k}\]with \(\mcI_j\) the index set required to get \(\bV^{(\htau)}_{:,j}\).

- Parameters

sales_taxes (numpy.ndarray) – \((\bV^{(\htau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

sales_taxes’s slice.

-

static

excises_computer(excises: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(174)¶\[\bV^{(\ctau)}_{:,j} = \sum_{k \in \mcI_j} \bV^{(\ctau)}_{:,k}\]with \(\mcI_j\) the index set required to get \(\bV^{(\ctau)}_{:,j}\).

- Parameters

excises (numpy.ndarray) – \((\bV^{(\ctau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

excises’s slice.

-

static

-

class

iamax.library.BalanceOfTrade¶ Accounting entity that consists in a given nation’s net exports.

-

static

budget_constraint_computer(budget_constraints: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(175)¶\[\mcr_j = \sum_{k=1}^{|\mcI_j|/2} \mcr_k - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \mcr_k\]where \(\mcI_j\) is by default asserted to be of even cardinality.

- Parameters

budget_constraints (numpy.ndarray) – \((\bmcr_k)_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

budget_constraints’s slice.

Important

This method relies on the structure of its argument, with exports concentrated in the first half of

budget_constraintsand imports in the second.- Example

>>> a = np.array([[4., 16., 3., 2.]]) >>> BalanceOfTrade.budget_constraint_computer( ... budget_constraints=a ... ) array([[15.]])

Let’s vectorize the above example

>>> (v := np.stack((a, a[:, ::-1]))) array([[[ 4., 16., 3., 2.]], [[ 2., 3., 16., 4.]]]) >>> BalanceOfTrade.budget_constraint_computer( ... budget_constraints=v ... ) array([[[ 15.]], [[-15.]]])

-

static

other_costs_computer(other_costs: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(176)¶\[v_{\ootau,\ j} = \sum_{k=1}^{|\mcI_j|/2} v_{\ootau,\ k} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} v_{\ootau,\ k}\]where \(\mcI_j\) is by default asserted to be of even cardinality.

- Parameters

other_costs (numpy.ndarray) – \((\bv_{\ootau,\ k})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

other_costs.

Important

This method relies on the structure of its argument, with exports concentrated in the first half of

other_costsand imports in the second.

-

static

net_surplus_computer(net_surplus: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(177)¶\[\pi_{j} = \sum_{k=1}^{|\mcI_j|/2} \pi_{k} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \pi_{k}\]where \(\mcI_j\) is by default asserted to be of even cardinality.

- Parameters

net_surplus (numpy.ndarray) – \((\bpi_{k})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

net_surplus.

Important

This method relies on the structure of its argument, with exports concentrated in the first half of

net_surplusand imports in the second.

-

static

gross_income_throughput_computer(gross_incomes_throughputs: np.ndarray)¶ s/e., \(1 \times 1\), denoted as

(178)¶\[\mcr_{\text{cum},\ j} = \sum_{k=1}^{|\mcI_j|/2} \mcr_{\text{cum},\ k} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \mcr_{\text{cum},\ k}\]where \(\mcI_j\) is by default asserted to be of even cardinality.

- Parameters

gross_incomes_throughputs (numpy.ndarray) – \((\bmcr_k)_{\text{cum},\ k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

gross_incomes_throughputs.

Important

This method relies on the structure of its argument, with exports concentrated in the first half of

gross_incomes_throughputsand imports in the second.

-

static

input_values_computer(input_values: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(179)¶\[\bmcV_{:,j} = \sum_{k=1}^{|\mcI_j|/2} \bmcV_{:,k} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \bmcV_{:,k}\]with \(\mcI_j\) the index set required to get \(\bmcV_{:,j}\), by default asserted to be of even cardinality.

- Parameters

input_values (numpy.ndarray) – \((\bmcV_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

input_values’s slice.

See also

\(\mcI\)’s archetype

_iidentifiers.- Example

>>> a = np.hstack(( ... x := np.arange(-2, 3)[:, None], ... m := np.ones_like(x), ... )) >>> a array([[-2, 1], [-1, 1], [ 0, 1], [ 1, 1], [ 2, 1]]) >>> BalanceOfTrade.input_values_computer(input_values=a) array([[-3], [-2], [-1], [ 0], [ 1]])

Let’s vectorize the above example.

>>> (v := np.stack((a, -2*a))) array([[[-2, 1], [-1, 1], [ 0, 1], [ 1, 1], [ 2, 1]], [[ 4, -2], [ 2, -2], [ 0, -2], [-2, -2], [-4, -2]]]) >>> BalanceOfTrade.input_values_computer(input_values=v) array([[[-3], [-2], [-1], [ 0], [ 1]], [[ 6], [ 4], [ 2], [ 0], [-2]]])

Yet another example with an odd number of trade components.

>>> a = np.hstack((x , np.ones_like(x), m)) >>> (v := np.stack((a, -a))) array([[[-2, 1, 1], [-1, 1, 1], [ 0, 1, 1], [ 1, 1, 1], [ 2, 1, 1]], [[ 2, -1, -1], [ 1, -1, -1], [ 0, -1, -1], [-1, -1, -1], [-2, -1, -1]]]) >>> BalanceOfTrade.input_values_computer(input_values=v) array([[[-2], [-1], [ 0], [ 1], [ 2]], [[ 2], [ 1], [ 0], [-1], [-2]]])

-

static

specific_margins_computer(specific_margins: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(180)¶\[\bV^{(\utau)}_{:,j} = \sum_{k=1}^{|\mcI_j|/2} \bV^{(\utau)}_{:,j} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \bV^{(\utau)}_{:,j}\]with \(\mcI_j\) the index set required to get \(\bV^{(\utau)}_{:,j}\), asserted to be of even cardinality.

- Parameters

specific_margins (numpy.ndarray) – \((\bV^{(\utau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

specific_margins’s slice.

-

static

trade_margins_computer(trade_margins: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(181)¶\[\bV^{(\jtau)}_{:,j} = \sum_{k=1}^{|\mcI_j|/2} \bV^{(\jtau)}_{:,j} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \bV^{(\jtau)}_{:,j}\]with \(\mcI_j\) the index set required to get \(\bV^{(\jtau)}_{:,j}\), asserted to be of even cardinality.

- Parameters

trade_margins (numpy.ndarray) – \((\bV^{(\jtau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

trade_margins’s slice.

-

static

sales_taxes_computer(sales_taxes: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(182)¶\[\bV^{(\htau)}_{:,j} = \sum_{k=1}^{|\mcI_j|/2} \bV^{(\htau)}_{:,j} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \bV^{(\htau)}_{:,j}\]with \(\mcI_j\) the index set required to get \(\bV^{(\htau)}_{:,j}\), asserted to be of even cardinality.

- Parameters

sales_taxes (numpy.ndarray) – \((\bV^{(\htau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

sales_taxes’s slice.

-

static

excises_computer(excises: np.ndarray)¶ s/e., \(|\mcI_j| \times 1\), denoted as

(183)¶\[\bV^{(\ctau)}_{:,j} = \sum_{k=1}^{|\mcI_j|/2} \bV^{(\ctau)}_{:,j} - \sum_{k=1 + |\mcI_j|/2}^{|\mcI_j|} \bV^{(\ctau)}_{:,j}\]with \(\mcI_j\) the index set required to get \(\bV^{(\ctau)}_{:,j}\), asserted to be of even cardinality.

- Parameters

excises (numpy.ndarray) – \((\bV^{(\ctau)}_{:,k})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI| \times |\mcI_j|\)

excises’s slice.

-

static

-

class

iamax.library.AQConserver¶ Class that captures the essence of the conservation law regarding additive quantities.

-

static

additive_output_volume_rooter(output_volume: np.ndarray, aggregated_input_volumes: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

(184)¶\[\approx 0\]- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.aggregated_input_volumes (numpy.ndarray) – \((\bq^{T,\text{drate}}_{k,1})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

aggregated_input_volumes’s slice.

- Example

>>> ovol = 10. >>> aivols = np.array([[6., 4.]]) >>> AQConserver.additive_output_volume_rooter( ... output_volume=ovol, aggregated_input_volumes=aivols, ... ) array([[0.]])

>>> vovol = np.array([[[ovol]], [[.5*ovol]]]) >>> vovol array([[[10.]], [[ 5.]]]) >>> vaivols = np.stack((aivols, .5*aivols[..., ::-1])) >>> vaivols array([[[6., 4.]], [[2., 3.]]]) >>> AQConserver.additive_output_volume_rooter( ... output_volume=vovol, aggregated_input_volumes=vaivols, ... ) array([[[0.]], [[0.]]])

-

static

-

class

iamax.library.SymmetricNodes¶ Class that captures the essence of entities balancing each other out through

gross_income_throughputattribute.-

static

gross_income_throughput_rooter(gross_incomes_throughputs: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

- Parameters

gross_incomes_throughputs (numpy.ndarray) – \((\bmcr_k)_{\text{cum},\ k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

gross_incomes_throughputs.- Example

>>> a = np.array([[.9, -.9]]) >>> SymmetricNodes.gross_income_throughput_rooter( ... gross_incomes_throughputs=a ... ) array([[0.]])

Let’s vectorize the above example.

>>> v = np.stack(( ... np.array([[.5, -.5]]), ... np.array([[.0, -.5]]), ... np.array([[.5, .0]]), ... )) >>> SymmetricNodes.gross_income_throughput_rooter( ... gross_incomes_throughputs=v ... ) array([[[ 0.]], [[ 1.]], [[-1.]]])

-

static

-

class

iamax.library.BalancedWorldTrade¶ Class that refers to the requirement in international economics that the sum of all trade balances across regions must equal zero. This identity reflects the idea that every export is matched by an import somewhere else, ensuring that total exports equal total imports when viewed globally.

Note

This class assumes that world trade is resolved in terms of physical volumes.

-

static

spendings_dfree_rooter(spendings_dfree: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

- Parameters

spendings_dfree (numpy.ndarray) – \((\bmcv_k)_{\neg\ttau,\ k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of

spendings_dfree.- Example

>>> a = np.array([[.9, -.9]]) >>> BalancedWorldTrade.spendings_dfree_rooter( ... spendings_dfree=a ... ) array([[0.]])

Let’s vectorize the above example.

>>> v = np.stack(( ... np.array([[.5, -.5]]), ... np.array([[.0, -.5]]), ... np.array([[.5, .0]]), ... )) >>> BalancedWorldTrade.spendings_dfree_rooter( ... spendings_dfree=v ... ) array([[[ 0.]], [[ 1.]], [[-1.]]])

-

static

Class that abstracts the idea of agents who jointly own 100% of an activity’s outstanding shares.

s/e., \(1 \times 1\) unit-dimensionless zero.

(185)¶\[\approx 0\]- Parameters

income_private_circuit_rsto (numpy.ndarray) – \((\obtheta_{k})_{k \in \mcI_j}\), i.e. a \(1 \times |\mcI_j|\) slice of

income_private_circuit_rsto.

See also

- Example

>>> a = np.array([[.9]]) >>> Shareholders.income_private_circuit_rsto_rooter( ... income_private_circuit_rsto=a ... ) array([[-0.1]])

Let’s vectorize the above example.

>>> (v := np.stack((a, 1 - a, a + .1))) array([[[0.9]], [[0.1]], [[1. ]]]) >>> Shareholders.income_private_circuit_rsto_rooter( ... income_private_circuit_rsto=v ... ) array([[[-0.1]], [[-0.9]], [[ 0. ]]])

-

class

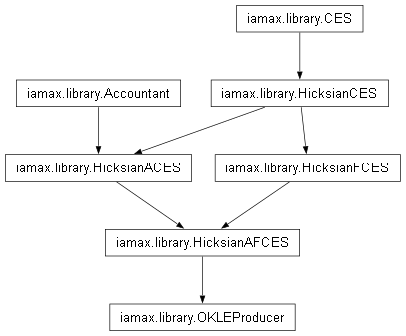

iamax.library.Accountant¶ Static class (to be inherited) that aggregates a bunch of methods related to accounting equations.

-

static

output_price_computer(*, output_volume: float, input_values: np.ndarray)¶ s/e., \(1 \times 1\).

(186)¶\[\up_j = \frac{\sum_{k \in \mcI_j} \mcv_k}{q_j}\]with \(\mcI_j\) the index set required to get \(\up_j\).

- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.

See also

- Example

>>> a = 1. >>> b = np.array([[1., 9.]]) >>> Accountant.output_price_computer( ... output_volume=a, input_values=b ... ) array([[10.]])

Let’s vectorize the above example

>>> Accountant.output_price_computer( ... output_volume=np.atleast_2d([a, 5*a]).T, ... input_values=np.vstack((b, b)) ... ) array([[10.], [ 2.]])

-

static

-

class

iamax.library.CoInitiatedVolumes(scaling_factor: float = 1.0)¶ Class that abstracts the concept of (independent) volumes whose initial state are yet to be determined jointly.

- Parameters

scaling_factor (float) – S/e. set to

1by default.

-

output_volumes_ccomputer(self, *, input_values: np.ndarray, additive_output_volumes: np.ndarray)¶ s/e.

- Parameters

additive_output_volumes (numpy.ndarray) – \(q_j\), i.e. the \(j\)ths \(1 \times 1\)

additive_output_volumes’s elements, whose last component only is of interest.input_values (numpy.ndarray) – \((\bmcV_{kk,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(|\mcI_j| \times |\mcI_j| + 1\)

input_values’s slice (diagonal) rectangular slice.

Important

This method relies on the structure of its argument, as outlined in the description of argument

additive_output_volumes.Attention

By appending its output with a 0, this method overwrites the last component of the targeted attribute.

-

class

iamax.library.BalancedSM¶ Class that abstracts the concept of specific margins summing to zero across consumers subjected to it.

-

static

specific_margin_balance_rooter(specific_margins_balances: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

- Parameters

specific_margins_balances (numpy.ndarray) – \(\bv_{\utau,\ j}\), i.e. the \(j\)th \(1 \times 1\) element of

specific_margins_balances.- Example

>>> a = np.array([[.9]]) >>> BalancedSM.specific_margin_balance_rooter( ... specific_margins_balances=a ... ) array([[0.9]])

Let’s vectorize the above example.

>>> v = np.stack(( ... np.array([[.5]]), ... np.array([[.0]]), ... np.array([[.5]]), ... )) >>> BalancedSM.specific_margin_balance_rooter( ... specific_margins_balances=v ... ) array([[[0.5]], [[0. ]], [[0.5]]])

-

static

-

class

iamax.library.InitiallyBalancedSM¶ BalancedSM’s counterpart that restricts the balancing at time t=0.-

static

specific_margin_balance_crooter(specific_margins_balances: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

- Parameters

specific_margins_balances (numpy.ndarray) – \(\bv_{\utau,\ j}\), i.e. the \(j\)th \(1 \times 1\)

specific_margins_balances’s element.- Example

>>> a = np.array([[.9]]) >>> InitiallyBalancedSM.specific_margin_balance_crooter( ... specific_margins_balances=a ... ) array([[0.9]])

Let’s vectorize the above example.

>>> v = np.stack(( ... np.array([[.5]]), ... np.array([[.0]]), ... np.array([[.5]]), ... )) >>> InitiallyBalancedSM.specific_margin_balance_crooter( ... specific_margins_balances=v ... ) array([[[0.5]], [[0. ]], [[0.5]]])

-

static

-

class

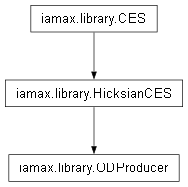

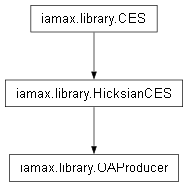

iamax.library.CES(sigma: float|tuple[float]|np.ndarray, nu: float|tuple[float]|np.ndarray = 1.0, eta: float|tuple[float]|np.ndarray = 0.0)¶ Constant Elasticity of Substitution base class and/or mixin class.

- Parameters

sigma (float or np.ndarray) – The elasticity of substitution \(\sigma\), with the substitution parameter being defined as \(\rho = \frac{\sigma - 1}{\sigma}\).

nu (float) – The degree of homogeneity of the aggregation \(\nu\), set to

1.by default.eta (float) – The responsiveness parameter \(\eta\), used under dynamic circumstances, if any. Set to

.0by default.

Note

This class can either be linear, Cobb–Douglas or Leontief:

If \((\sigma \to \infty) \iff (\rho \to 1)\), we get a linear or perfect substitutes function;

If \((\sigma \to 1) \iff (\rho \to 0)\), we get a Cobb–Douglas function;

If \((\sigma \to 0) \iff (\rho \to -\infty)\), we get a Leontief or perfect complements function.

- Example

>>> CES(sigma=0).aggregation_type 'Leontief' >>> CES(sigma=.5).aggregation_type 'Gross complements' >>> CES(sigma=1).aggregation_type 'Cobb–Douglas' >>> CES(sigma=2).aggregation_type 'Imperfect Substitutes' >>> CES(sigma=np.inf).aggregation_type 'Perfect substitutes' >>> CES(sigma=[0, 1, np.inf]).aggregation_type ['Leontief', 'Cobb–Douglas', 'Perfect substitutes']

-

property

aggregation_type(self)¶ Aggregation qualifier, be this aggregation related to cardinal (e.g. production) or ordinal (e.g. utility level) quantities.

- Example

>>> CES(sigma=[0, 1, np.inf]).aggregation_type ['Leontief', 'Cobb–Douglas', 'Perfect substitutes']

-

property

sigma(self)¶ Elasticity of substitution \(\sigma\).

-

property

rho(self)¶ Substitution parameter \(\rho\).

-

property

nu(self)¶ Aggregation’s degree of homogeneity \(\nu\).

-

property

eta(self)¶ Responsiveness to input price changes \(\eta\).

-

abstract

compute_calibrand_0(self, **kwargs: float)¶ Method to be called during calibration.

Attention

This method is assumed (but not asserted) to only be dealing with Keyword-Only Arguments.

Warning

This method will likely be reattached as soon as a technology (or preference) morphism being ontologically upstream of

CESis defined.

-

static

_aggregator(*, shares: np.ndarray, aggregands: np.ndarray, rho: float, nu_rho_inv: float)¶ Class’s core morphism, \(1 \times 1\), denoted as

(187)¶\[y = \left( \sum_{i=1}^n a_{i} x_{i}^{\rho} \right)^\frac{\nu}{\rho}\]where \(y\) is the quantity of aggregate, \(x_i\) the quantity of \(i\)-aggregand, \(a_i\) its associated share, \(\rho\) the substitution parameter and \(\nu\) the degree of homogeneity of the aggregation.

Note

This method is vectorization friendly over the 0th axis. Incidentally, it may also be turned into instance method once the developments stabilize.

- Parameters

shares (numpy.ndarray) – \(1 \times n\) archetype of the distribution parameters.

aggregands (numpy.ndarray) – \(1 \times n\) archetype of the aggregands.

rho (float) – \(1 \times 1\) archetype of the substitution parameter.

nu_rho_inv (float) – Precomputed \(1 \times 1\) archetype of aggregation degree of homogeneity multiplied by the inverse of the substitution parameter.

- Example

>>> a = np.array([[0.29151, 0.95657]]) >>> b = np.array([[1782.232, 19190.896]]) >>> CES._aggregator( ... shares=a, aggregands=b, ... rho=.5, nu_rho_inv=2. ... ) array([[20973.22]])

Let’s vectorize the above example

>>> CES._aggregator( ... shares=np.vstack((a, a)), ... aggregands=np.vstack((b, b)), ... rho=np.atleast_2d([.5, .0]).T, ... nu_rho_inv=2. ... ) array([[2.10e+04], [1.56e+00]])

-

class

iamax.library.HicksianCES(*args, **kwargs)¶

Constant Elasticity of Substitution abstraction whose optimal demand function derives from a maximization program formulated à la Hicks.

Note

Calculations assert constant return to scale, i.e. Eq.187’s \(\nu\) is forced to be \(1\) at instantiation.

-

compute_calibrand_0(self, *, output_volume: float|np.ndarray, input_volumes: np.ndarray, input_values: np.ndarray)¶ This method supports the FOC-based calibration of \((a_{k,j})_{k \in \mcI_j}\), the \(|\mcI_j|\) demand distribution parameters related to aggregate \(j\),

(188)¶\[a_k = \left[ \left( \frac{\mcv_k}{\sum_{k' \in \mcI_j} \mcv_{k'}} \right)^{ \text{I}(\rho_j \neq -\infty) } \left(\frac{q_j}{q_k}\right)^{ \rho_j^{\text{I}(\rho_j \neq -\infty)} } \right]^{\text{I}(\rho_j \neq 1)}, \ \forall k \ \in \mcI_j\]with \(q_j\) the output level to be satisfied, \(\rho_j\) the substitution parameter, \(\mcI_j\) the index set of inputs required by \(q_j\)’s underlying technology, \(q_k\) the optimal level of input required to meet \(q_j\), \(\mcv_k\) the \(q_k\)’s input value and \(\text{I}(\cdot)\) an indicator function returning the trueness of the statement being passed as argument.

- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.input_volumes (numpy.ndarray) – \((\bQ_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes’s slice.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.

- Example

>>> ovol = 20973.128 >>> ivols = np.array([[1782.232, 19190.896]]) >>> ivals = 1e3*ivols

>>> h = HicksianCES(sigma=2.) >>> _ = h.compute_calibrand_0( ... output_volume = ovol, ... input_volumes = ivols, ... input_values = ivals, ... ) >>> h.calibrand_0 array([[0.29, 0.96]])

Let’s illustrate how such calculation can be vectorized along the 0th axis.

>>> vovol = np.array([[[ovol]], [[ovol]]]) >>> vivols = np.stack((ivols, .1*ivols)) >>> vivals = 1e3*vivols

>>> h.compute_calibrand_0( ... output_volume = vovol, ... input_volumes = vivols, ... input_values = vivals, ... ).calibrand_0 array([[[0.29, 0.96]], [[0.92, 3.02]]])

The non-constant instantiation parameters case follows.

>>> h = HicksianCES(sigma=[[[2.]], [[3.]]]) >>> _ = h.compute_calibrand_0( ... output_volume = vovol, ... input_volumes = vivols, ... input_values = vivals, ... ) >>> h.calibrand_0 array([[[0.29, 0.96]], [[2.04, 4.51]]])

See also

-

compute_calibrand_0_star(self, *, ioq_shares_drates: np.ndarray, ioq_shares_drates2: np.ndarray, ioq_productivities_drates: np.ndarray, ioq_productivities_drates2: np.ndarray)¶ Define

calibrand_0_star, i.e. a version ofcalibrand_0that internalizes (crises-like) shocks,(189)¶\[\begin{split}a_k^{*} &= a_k \left( 1 + \beta^{\text{drate}}_k + \beta^{\text{drate}^{ii}}_k \right)^{ \rho_j^{\text{I}(\rho_j \neq -\infty)} \text{I}(\rho_j \neq 1) } \\ & \left( 1 + \alpha^{-1,\ \text{drate}}_k + \alpha^{-1,\ \text{drate}^{ii}}_k \right)^{\text{I}(\rho_j = -\infty)}, \ \forall k \ \in \mcI_j\end{split}\]where \(a_k\) and \(\rho_j\) are as defined in Eq.188, \(\beta^\text{drate}_k\) and \(\beta^{\text{drate}^{ii}}_k\) are respectively a crisis-like shock and a spread from it, \(\alpha^{-1,\ \text{drate}^{ii}}_k\) and \(\alpha^{-1,\ \text{drate}}_k\) are, respectively, a scenarized productivity (discrete) growth and a spread from it.

- Parameters

ioq_shares_drates (numpy.ndarray) – \((\bbeta^\text{drate}_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_shares_drates’s slice.ioq_shares_drates2 (numpy.ndarray) – \((\bbeta^{\text{drate}^{ii}}_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_shares_drates2’s slice.ioq_productivities_drates (numpy.ndarray) – \((\balpha^{-1,\ \text{drate}_{k,j}})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_productivities_drates’s slice.ioq_productivities_drates2 (numpy.ndarray) – \((\balpha^{-1,\ \text{drate}^{ii}_{k,j}})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_productivities_drates2’s slice.

Note

ioq_productivities_drateshas vocation to “overwrite”ioq_shares_dratessooner or later.Important

Keep in mind that \(a_k\) and \(\rho_j\) are internally handled as instance attributes, i.e. in the same manner as

calibrand_0andrho.

Alleged input shares, \(1 \times |\mcI_j|\), denoted as

where \(\eta_j\) is a \(j\)-specific responsiveness parameter and \(\mcI_j\) and \(p_k\) are as described in Eq.194.

- Parameters

input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.input_prices_lagged (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of the lagged version of

input_prices.ioq_intensities_lagged (numpy.ndarray) – \((\balpha_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of the lagged version of

ioq_intensities.

- Example

>>> invariants = dict( ... input_prices = np.array([[1., 1.25]]), ... input_prices_lagged = np.array([[1., 1.]]), ... ioq_intensities_lagged = np.array([[.4, .6]]), ... )

>>> HicksianCES( ... sigma=np.inf, eta=0. ... ).allege_input_shares(**invariants).alleged_input_shares array([[0.4, 0.6]]) >>> HicksianCES( ... sigma=np.inf, eta=1. ... ).allege_input_shares(**invariants).alleged_input_shares array([[0.35, 0.65]]) >>> HicksianCES( ... sigma=np.inf, eta=4. ... ).allege_input_shares(**invariants).alleged_input_shares array([[0.21, 0.79]])

-

compute_input_volumes_shocks(self, *, input_volumes_drates: np.ndarray)¶ s/e., \(1 \times |\mcI_j|\), calculated and assigned to attribute

input_volumes_shockssince required in several methods of the instance.(191)¶\[\bQ^\text{dmult}_j = 1 + \bQ^\text{drate}_j\]- Parameters

input_volumes_drates (numpy.ndarray) – \((\bQ^\text{drate}_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes_drates’s slice.

Note

Since the name of this method mirrors nothing within the list of eligible variables (be them related to targets or arguments), it will be assumed to work in place.

Important

Keep in mind that

input_volumes_shocksis defined and internally handled as instance attributes, cf. the example section below.- Example

>>> h = HicksianCES(sigma=None) >>> h.compute_input_volumes_shocks( ... input_volumes_drates=np.array([[.1, .2]]) ... ).input_volumes_shocks array([[1.1, 1.2]])

-

_output_volume_computer(self, *, input_volumes: np.ndarray)¶ Output supply, \(1 \times 1\), denoted as

(192)¶\[q_j = \left( \sum_{k \in \mcI_j} a_k q_k^{ \rho_j^{ \text{I}(\rho_j\neq-\infty) } } \right)^{ \rho_j^{ -\text{I}(\rho_j\neq-\infty) } } |\mcI_j|^{ -\text{I}(\rho_j=-\infty) }\]where \(\mcI_j\), \(q_j\), \(q_k\), \(a_k\), \(\rho_j\) and \(\text{I}(\cdot)\) are as described in Eq.188.

Note

Eq.192 is unconditionally valid only when \(q_{k=1, \ldots, |\mcI_j|}\)’s levels are the optimal input demands’.

- Parameters

input_volumes (numpy.ndarray) – \((\bQ_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes’s slice.- Example

>>> ovol = 20973.128 >>> ivols = np.array([[1782.232, 19190.896]]) >>> ivals = 1e3*ivols

>>> h = HicksianCES(sigma=2.) >>> _ = h.compute_calibrand_0( ... output_volume = ovol, ... input_volumes = ivols, ... input_values = ivals ... ) >>> h._output_volume_computer( ... input_volumes = ivols, ... ) array([[20973.13]])

Let’s illustrate how such calculation can be vectorized along the 0th axis.

>>> vovol = np.array([[[ovol]], [[.5*ovol]], [[ovol]]]) >>> vivols = np.stack((ivols, .5*ivols, ivols)) >>> vivals = 1e3*vivols

>>> _ = h.compute_calibrand_0( ... output_volume = vovol, ... input_volumes = vivols, ... input_values = vivals, ... ) >>> h._output_volume_computer( ... input_volumes = vivols, ... ) array([[[20973.13]], [[10486.56]], [[20973.13]]])

-

compute_output_price_driver(self, *, output_price_drate: np.ndarray)¶ s/e.

-

output_price_computer(self, *, input_prices: np.ndarray)¶ s/e., \(1 \times 1\).

(193)¶\[\up_j = \left( \sum_{k \in \mcI_j} \left[ a_k^{ (-1)^{\text{I}(\sigma_j = 0)} \sigma_j^{\text{I}(\sigma_j \neq 0)} } \right]^{\text{I}(\sigma_j \neq \infty)} p_k^{ (1 - \sigma_j)^{\text{I}(\sigma_j \neq \infty)} } s_k^{\text{I}(\sigma_j = \infty)} \right)^{ (1 - \sigma_j)^{-\text{I}(\sigma_j \neq \infty)} }\]where \(\mcI_j\), \(a_k\) and \(\text{I}(\cdot)\) are as in Eq.188, \(\sigma_j\) and \(p_k\) are as in Eq.194, \(\up_j\) is the output’s producer price and \(s_k\) is as in Eq.190.

- Parameters

input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.

See also

Important

This method overrides its (parent)

output_price_computercounterpart.- Example

>>> ovol = 20973.128 >>> ivols = np.array([[1782.232, 19190.896]]) >>> iprcs = np.array([[1000., 1000.]]) >>> ivals = iprcs*ivols

>>> h = HicksianCES(sigma=2.) >>> _ = h.compute_calibrand_0( ... output_volume = ovol, ... input_volumes = ivols, ... input_values = ivals, ... ) >>> h.output_price_computer( ... input_prices = iprcs, ... ).item() 1000.0

Let’s illustrate how such calculation can be vectorized over the 0th axis.

>>> vovol = np.array([[[ovol]], [[.5*ovol]], [[ovol]]]) >>> vivols = np.stack((ivols, .5*ivols, ivols)) >>> vivals = 1e3*vivols >>> viprcs = 1e3*np.ones_like(vivols)

>>> _ = h.compute_calibrand_0( ... output_volume = vovol, ... input_volumes = vivols, ... input_values = vivals, ... ) >>> h.output_price_computer( ... input_prices = viprcs, ... ) array([[[1000.]], [[1000.]], [[1000.]]])

-

input_volumes_computer(self, *, output_volume: float|np.ndarray, input_prices: np.ndarray)¶ Input demands, \(1 \times |\mcI_j|\), denoted as

(194)¶\[\begin{split}q_k &= q_j \left[ \alpha_k \left(\frac{\up_j}{p_k}\right)^{\sigma_j} \right]^{\text{I}(\sigma_j \neq \infty)} \left[s_k\right]^{\text{I}(\sigma_j = \infty)} \\ &= q_j \left[ \alpha_k p_k^{-\sigma_j} \left( \sum_{k' \in \mcI_j} \alpha_{k'} p_{k'}^{1 - \sigma_j} \right)^{ \frac{\sigma_j}{1 - \sigma_j} } \right]^{\text{I}(\sigma_j \neq \infty)} \left[s_k\right]^{\text{I}(\sigma_j = \infty)}, \ \forall k \ \in \mcI_j\end{split}\]where \(\alpha_k=a_k^{(-1)^{\text{I}(\sigma_j = 0)} \sigma_j^{\text{I}(\sigma_j \neq 0)}}\) and \(\mcI_j\), \(q_j\), \(q_k\), \(a_k\) and \(\text{I}(\cdot)\) are as in Eq.188, \(p_k\) is the \(q_k\)’s price and \(s_k\) is as described in Eq.190.

- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.

- Example

>>> ovol = 20973.128 >>> ivols = np.array([[1782.232, 19190.896]]) >>> iprcs = np.array([[1000., 1000.]]) >>> ivals = iprcs*ivols

>>> h = HicksianCES(sigma=2) >>> _ = h.compute_calibrand_0( ... output_volume = ovol, ... input_volumes = ivols, ... input_values = ivals, ... ) >>> h.input_volumes_computer( ... output_volume = ovol, ... input_prices = iprcs, ... ) array([[ 1782.23, 19190.9 ]])

Let’s illustrate how such calculation can be vectorized over the 0th axis.

>>> h = HicksianCES(sigma=[[[2.]], [[2.]], [[.5]]]) >>> vovol = np.array([[[ovol]], [[ovol]], [[ovol]]]) >>> vivols = np.stack((ivols, ivols[:, ::-1], ivols)) >>> vivals = 1e3*vivols >>> viprcs = 1e3*np.ones((3, 1, 2))

>>> h.compute_calibrand_0( ... output_volume = vovol, ... input_volumes = vivols, ... input_values = vivals, ... ).input_volumes_computer( ... output_volume = vovol, ... input_prices = viprcs, ... ) array([[[ 1782.23, 19190.9 ]], [[19190.9 , 1782.23]], [[ 1782.23, 19190.9 ]]])

Once again, but moving away from the calibration context regarding relative prices.

>>> viprcs[..., 0] *= .5 >>> h.input_volumes_computer( ... output_volume = vovol, ... input_prices = viprcs, ... ) array([[[ 6055.96, 16302.5 ]], [[20931.83, 485.98]], [[ 2457.72, 18713.25]]])

-

-

class

iamax.library.HicksianICES(*args, **kwargs)¶

Ordinal-production altered version of

HicksianCES.Important

At the moment, this method cannot be instantiated at \(\sigma \to \infty\) since it would require

MSystemto be endowed with a new economic attribute k.a. iwq_intensities.-

compute_calibrand_0(self, *, ordinal_volume: float|np.ndarray, input_volumes: np.ndarray, input_values: np.ndarray)¶ s/e.

See also

LSP-offending (in-place) computer.

See also

The reason why this method is nullified.

- Example

>>> HicksianICES.allege_input_shares() Traceback (most recent call last): ... NotImplementedError: Require `core.MSystem.iwq_intensities`

-

ordinal_volume_computer(self, *, input_volumes: np.ndarray)¶ s/e.

See also

-

input_volumes_computer(self, *, ordinal_volume: float|np.ndarray, input_prices: np.ndarray)¶ s/e.

-

-

class

iamax.library.HicksianPICES(*args, scaling_factor: float = 1.0, **kwargs)¶

Augmented version of

HicksianICESthat also computes the price of the ordinal quantities being generated.- Parameters

scaling_factor (float) – Ordinal price scaling factor. To

1by default.

-

compute_ordinal_price_driver(self, *, ordinal_price_drate: np.ndarray)¶ s/e.

-

ordinal_price_computer(self, *, input_prices: np.ndarray)¶ s/e.

-

class

iamax.library.ScHicksianCES¶

HicksianCES’s altered version whose calibrands determination is solver based.-

compute_calibrand_0(self, *, ioq_intensities_drates: np.ndarray)¶ s/e.

-

ioq_intensities_drates_crooter(self, *, input_volumes: np.ndarray, input_prices: np.ndarray)¶ s/e.

-

-

class

iamax.library.SmHicksianCES¶

HicksianCES’s altered version whose calibrands determination is softmax-based.-

compute_calibrand_0(self, *, input_prices: np.ndarray, input_volumes: np.ndarray)¶ This method supports the softmax-derived calibration of \((a_{k,j})_{k \in \mcI_j}\), the \(|\mcI_j|\) demand distribution parameters related to aggregate \(j\),

(195)¶\[a_k = \left[ \frac{ p_{k}q_{k}^{1/\sigma_j} }{ \sum_{k' \in \mcI_j} p_{k'}q_{k'}^{1/\sigma_j} } \right]^{\text{I}(\sigma_j \neq \infty)}, \ \forall k \ \in \mcI_j\]with \(\sigma_j\) the elasticity of substitution, \(\mcI_j\) the index set of inputs required by \(q_j\)’s underlying technology, \(q_k\) the optimal level of input required to meet \(q_j\), \(p_k\) the \(q_k\)’s associated input price and \(\text{I}(\cdot)\) an indicator function returning the trueness of the statement being passed as argument.

- Parameters

input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.input_volumes (numpy.ndarray) – \((\bQ_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes’s slice.

-

-

class

iamax.library.HicksianFCES¶

HicksianCES’s altered version whose underlying trade-off is forced.LSP-offending (in-place) computer.

-

aggregated_input_volumes_rooter(self, *, output_volume: np.ndarray, input_volumes: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

(196)¶\[\approx 0\]- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.input_volumes (numpy.ndarray) – \((\bQ_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes’s slice.

See also

-

class

iamax.library.HicksianACES¶

HicksianCES’s altered version whose costs calculation is based on accounting rules.

-

class

iamax.library.HicksianAFCES¶

HicksianACES’s altered version whose underlying trade-off is forced.

-

class

iamax.library.HicksianGAFCES(*args, negated_mask: bool = False, **kwargs)¶

HicksianACES’s altered version whose underlying trade-off is forced in a generalized manner by restricting it to a consumption subset of arbitrary size.- Parameters

negated_mask (bool) – Whether the mask passed as argument

input_volumes_drates2of the methodcompute_calibrand_0is to be negated. Argumentinput_volumes_drates2indeed boolean-specifies the goods being freely subject to trade-off by default. Set toFalseby default.

Attention

This class isn’t well tested for

sigma!=0cases yet, which condition is not asserted (!)-

compute_calibrand_0(self, *, output_volume: float|np.ndarray, input_values: np.ndarray, input_volumes: np.ndarray, input_volumes_drates2: np.ndarray)¶ Altered version of

compute_calibrand_0.- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.input_volumes (numpy.ndarray) – \((\bQ_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes’s slice.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.input_volumes_drates2 (numpy.ndarray) – \((\bQ^\text{drate}_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes_drates2’s slice.

- Example

>>> ovol = 20973.128 >>> ivols = np.array([[1782.232, 19190.896]]) >>> ivals = 1e3*ivols >>> imsks = np.array([[1, 0]])

>>> h = HicksianGAFCES(sigma=0, negated_mask=False) >>> _ = h.compute_calibrand_0( ... output_volume = ovol, ... input_volumes = ivols, ... input_values = ivals, ... input_volumes_drates2 = imsks, ... ) >>> h.calibrand_0 array([[11.77, 1.09]]) >>> h._volumes_mask array([[ True, False]])

See also

-

compute_calibrand_0_star(self, *, output_volume: np.ndarray, input_values: np.ndarray, input_volumes: np.ndarray, ioq_shares_drates: np.ndarray = 0.0, ioq_shares_drates2: np.ndarray = 0.0, ioq_productivities_drates: np.ndarray = 0.0, ioq_productivities_drates2: np.ndarray = 0.0)¶ Augmented version of

compute_calibrand_0_star()that integrates the information related to consumptions forcing.- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.ioq_shares_drates (numpy.ndarray) – \((\bbeta^\text{drate}_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_shares_drates’s slice. Set to.0by default.ioq_shares_drates2 (numpy.ndarray) – \((\bbeta^{\text{drate}^{ii}}_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_shares_drates2’s slice. Set to.0by default.ioq_productivities_drates (numpy.ndarray) – \((\balpha^{-1,\ \text{drate}_{k,j}})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_productivities_drates’s slice. Set to.0by default.ioq_productivities_drates2 (numpy.ndarray) – \((\balpha^{-1,\ \text{drate}^{ii}_{k,j}})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_productivities_drates2’s slice. Set to.0by default.

- Example

>>> ovol = 20973.128 >>> ivols = np.array([[1782.232, 19190.896]]) >>> iprcs = np.array([[1000., 1000.]]) >>> ivals = iprcs*ivols >>> imsks = np.array([[0, 1]]) >>> h = HicksianGAFCES(sigma=.0, negated_mask=False) >>> h.aggregation_type 'Leontief'

>>> h.compute_calibrand_0( ... output_volume = ovol, ... input_volumes = ivols, ... input_values = ivals, # † ... input_volumes_drates2 = imsks, ... ).calibrand_0 array([[11.77, 1.09]]) >>> ivôls = h.input_volumes_computer( ... output_volume = ovol, ... input_prices = iprcs, # † ... ) >>> ivôls array([[ 1782.23, 19190.9 ]]) >>> h._output_volume_computer(input_volumes=ivôls) array([[20973.13]])

Let’s now force the first good’s level of consumption by editing its market configuration.

>>> h.compute_calibrand_0_star( ... output_volume = ovol, ... input_volumes = ivols * np.array([[.5, 2.]]), ... input_values = ivals, # † ... ).calibrand_0 array([[23.54, 1.09]]) >>> ivôls = h.input_volumes_computer( ... output_volume = ovol, ... input_prices = iprcs * np.array([[2., .5]]), # † ... ) >>> ivôls array([[ 891.12, 19190.9 ]]) >>> h._output_volume_computer(input_volumes=ivôls) array([[20973.13]])

† : put aside in the

sigma=0case ; maintained in anticipation of a futuresigma-related generalization.

See also

Alleged input shares, \(1 \times |\mcI_j|\).

- Parameters

input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.input_prices_lagged (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of the lagged version of

input_prices.ioq_intensities (numpy.ndarray) – \((\balpha_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

ioq_intensities’s slice.ioq_intensities_lagged (numpy.ndarray) – \((\balpha_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\) slice of the lagged version of

ioq_intensities.

- Example

>>> invariants = dict( ... input_prices = np.array([[1., 1.25, 1.]]), ... input_prices_lagged = np.array([[1., 1., 1.]]), ... ioq_intensities = np.array([[.5, .4, .1]]), ... ioq_intensities_lagged = np.array([[.6, .2, .2]]), ... ) >>> h = HicksianGAFCES(sigma=np.inf, eta=.0, negated_mask=False)

>>> h._volumes_mask = np.array([[1, 1, 1]]).astype(bool) >>> h.allege_input_shares(**invariants).alleged_input_shares array([[0.6, 0.2, 0.2]])

>>> h._volumes_mask = np.array([[0, 1, 1]]).astype(bool) >>> h.allege_input_shares(**invariants).alleged_input_shares array([[0.5 , 0.25, 0.25]])

>>> h._volumes_mask = np.array([[0, 0, 1]]).astype(bool) >>> h.allege_input_shares(**invariants).alleged_input_shares array([[0.5, 0.4, 0.1]])

>>> h._volumes_mask = np.array([[0, 0, 0]]).astype(bool) >>> h.allege_input_shares(**invariants).alleged_input_shares array([[0.5, 0.4, 0.1]])

Attention

allege_input_shares’s right stochasticity is a priori not effective as~._volumes_maskturns allFalse(orTrueifnegated_mask=True).See also

-

class

iamax.library.HicksianRGAFCES¶

s/e.

-

aggregated_input_volumes_rooter(self, *, output_volume: np.ndarray, input_volumes: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

(197)¶\[\approx 0\]- Parameters

output_volume (float) – \(q_j\), i.e. the \(j\)th \(1 \times 1\)

output_volumes’s element.input_volumes (numpy.ndarray) – \((\bQ_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes’s slice.

See also

-

-

class

iamax.library.HicksianFLUMRS(*args, **kwargs)¶

Unit MRS linear (forced) production function which boils down to a special case of

HicksianFCESwhere \(a_k=1 \text{ for } k \in \mcI_j\) and \(\sigma \longrightarrow \infty\).Note

This class’s

compute_calibrand_0()has no system-dependence since the underlying calibrands are inherently equal to \(1\).

-

class

iamax.library.MarshallianCES(*args, **kwargs)¶

Constant Elasticity of Substitution abstraction whose optimal demand function derives from a maximization program formulated à la Marshall.

Note

Calculations assert constant return to scale, i.e. Eq.187’s \(\nu\) is forced to be \(1\) at instantiation.

-

compute_calibrand_0(self, *, budget_constraint: float, input_values: np.ndarray)¶ Calibrate the \((a_{k,j})_{k \in \mcI_j}\), i.e. the \(|\mcI_j|\) demand share parameters related to aggregate \(j\), considering them equal to the budget share of each of the underlying consumptions in the base year.

(198)¶\[a_k = \frac{\mcv_k}{r_j}, \ \forall k \ \in \mcI_j\]with \(r_j\) the budget constraint to be saturated, \(\mcI_j\) the index set of the subject-to-\(r_j\) traded off consumptions, \(\mcv_k\) the \(q_k\)’s corresponding input value.

- Parameters

budget_constraint (float) – \(r_j\), i.e. the \(j\)th \(1 \times 1\)

budget_constraints’s element.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.

- Example

>>> m = MarshallianCES(sigma=None) >>> _ = m.compute_calibrand_0( ... budget_constraint=200., ... input_values=np.array([[110., 90.]]) ... ) >>> m._shares_sum array([[1.]]) >>> m.calibrand_0 array([[0.55, 0.45]])

>>> _ = m.compute_calibrand_0( ... budget_constraint=100., ... input_values=np.array([[110., 90.]]) ... ) >>> m._shares_sum array([[2.]]) >>> m.calibrand_0 array([[0.55, 0.45]])

See also

-

budget_constraint_crooter(self)¶ compute_calibrand_0()’s companion unit-dimensionless zero aiming at ensuring that the sum of shares add up to 1, \(1 \times 1\).- Example

>>> budc = 200. >>> ivals = np.array([[110., 90.]]) >>> m = MarshallianCES(sigma=None) >>> _ = m.compute_calibrand_0( ... budget_constraint=budc, input_values=ivals ... ) >>> m.budget_constraint_crooter() array([[0.]])

Let’s then illustrate how such calculation can be vectorized.

>>> vbudc = np.array([[[.5*budc]], [[budc]], [[2*budc]]]) >>> vivals = np.stack((ivals, ivals, ivals)) >>> m.compute_calibrand_0( ... budget_constraint=vbudc, input_values=vivals ... ).budget_constraint_crooter() array([[[ 1. ]], [[ 0. ]], [[-0.5]]])

-

input_volumes_computer(self, *, budget_constraint: float, input_prices: np.ndarray)¶ Input demands, \(1 \times |\mcI_j|\), denoted as

(199)¶\[q_k = \frac{ r_j p_{k}^{\frac{1}{\rho_j - 1}} }{ \sum_{k^{'} \in \mcI_j} p_{k^{'}}^{\frac{\rho_j}{\rho_j - 1}} \left[ \frac{a_k}{a_{k^{'}}} \right]^{\frac{1}{\rho_j - 1}} } = \frac{r_j}{ p_{k}^{\sigma_j} \sum_{k^{'} \in \mcI_j} p_{k^{'}}^{1-\sigma_j} \left[ \frac{a_{k^{'}}}{a_{k}} \right]^{\sigma_j} } \ \forall k \ \in \mcI_j\]where \(r_j\) is the budget constraint to be saturated, \(\rho_j = \frac{\sigma_j - 1}{\sigma_j}\) the substitution parameter, \(\sigma_j = \frac{1}{1 - \rho_j}\) the elasticity of substitution, \(\mcI_j\) the index set of consumptions traded off under \(r_j\), \(p_k\) the \(q_k\)’s price and \(a_k\) as in Eq.198.

See also

A two-good version of Eq.199 can be found in the notes prepared for the GAMS workshop on general equilibrium held in December 1995 in Boulder, Colorado.

What happens internally, is actually performed in matrix terms (so as to benefit from vectorization) as follows:

(200)¶\[\bq = \frac{r_j}{ \bp^{\sigma_j} \odot \mathbf{1}_{|\mcI_j|} \left( \bp^{1 - \sigma_j} \odot \left[ \ba \cdot \frac{1}{\ba^{'}} \right]^{\sigma_j} \right)^{'} }\]where \(\mathbf{1}_{|\mcI_j|}\), \(\bq = (q_1, \ldots, q_{|\mcI_j|})\), \(\ba = (a_1, \ldots, a_{|\mcI_j|})\) and \(\bp = (p_1, \ldots, p_{|\mcI_j|})\) are \(1 \times |\mcI_j|\) vectors.

- Parameters

budget_constraint (float) – \(r_j\), i.e. the \(j\)th \(1 \times 1\)

budget_constraints’s element.input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.

- Example

Let’s directly deal with the \(\rho_j=0 \iff \sigma_j=1\) CES’s limiting case, which makes it boil down down to a Cobb-Douglas function.

>>> budc = 200. >>> ivals = np.array([[110., 90.]]) >>> iprcs = np.array([[.9, 1.1]])

>>> m = MarshallianCES(sigma=1) >>> _ = m.compute_calibrand_0( ... budget_constraint=budc, input_values=ivals ... ) >>> m.calibrand_0 array([[0.55, 0.45]])

>>> m.input_volumes_computer( ... budget_constraint=budc, input_prices=np.ones_like(ivals), ... ) array([[110., 90.]]) >>> m.input_volumes_computer( ... budget_constraint=budc, input_prices=iprcs, ... ) array([[122.22, 81.82]])

You can check for yourself via, say, there. Let’s then illustrate how such calculation can be vectorized.

>>> vbudc = np.array([[[.5*budc]], [[budc]], [[2*budc]]]) >>> vivals = np.stack((ivals, ivals, ivals)) >>> viprcs = np.stack((iprcs, iprcs, iprcs))

>>> m = MarshallianCES(sigma=[[[2.]], [[1.]], [[.5]]]) >>> _ = m.compute_calibrand_0( ... budget_constraint=vbudc, input_values=vivals ... ) >>> m.calibrand_0 array([[[0.55, 0.45]], [[0.55, 0.45]], [[0.55, 0.45]]]) >>> m.input_volumes_computer( ... budget_constraint=vbudc, input_prices=viprcs, ... ) array([[[ 71.79, 32.17]], [[122.22, 81.82]], [[222.22, 181.82]]])

-

-

class

iamax.library.MarshallianGFCES(*args, negated_mask: bool = False, **kwargs)¶

MarshallianCES’s altered version whose underlying trade-off is forced in a generalized manner by restricting it to a consumption subset of arbitrary size.- Parameters

negated_mask (bool) – Whether the mask passed as argument

input_volumes_drates2of the methodcompute_calibrand_0is to be negated. Argumentinput_volumes_drates2indeed boolean-specifies the good being subject to consumption tradeoff by default. Set toFalseby default.

-

compute_calibrand_0(self, *, budget_constraint: float, input_values: np.ndarray, input_volumes_drates2: np.ndarray)¶ s/e.

- Parameters

budget_constraint (float) – \(r_j\), i.e. the \(j\)th \(1 \times 1\)

budget_constraints’s element.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.input_volumes_drates2 (numpy.ndarray) – \((\bQ^\text{drate}_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes_drates2’s slice. This variable is coerced into boolean and used as mask.

- Example

>>> m = MarshallianGFCES(sigma=None, negated_mask=False) >>> m.compute_calibrand_0( ... budget_constraint = 200., ... input_values = np.array([[110., 90.]]), ... input_volumes_drates2 = np.array([[1., 1.]]) ... ) >>> m._shares_sum array([[1.]]) >>> m.calibrand_0 array([[0.55, 0.45]])

>>> m.compute_calibrand_0( ... budget_constraint = 200., ... input_values = np.array([[110., 90.]]), ... input_volumes_drates2 = np.array([[1., 0.]]) ... ) >>> m._shares_sum array([[1.]]) >>> m.calibrand_0 array([[1., 0.]])

>>> m = MarshallianGFCES(sigma=None, negated_mask=True) >>> m.compute_calibrand_0( ... budget_constraint = 200., ... input_values = np.array([[110., 90.]]), ... input_volumes_drates2 = np.array([[0., 0.]]) ... ) >>> m._shares_sum array([[1.]]) >>> m.calibrand_0 array([[0.55, 0.45]])

>>> m.compute_calibrand_0( ... budget_constraint = 200., ... input_values = np.array([[110., 90.]]), ... input_volumes_drates2 = np.array([[1., 0.]]) ... ) >>> m._shares_sum array([[1.]]) >>> m.calibrand_0 array([[0., 1.]])

See also

-

input_volumes_computer(self, budget_constraint: float, input_values: np.ndarray, input_prices: np.ndarray)¶ s/e.

- Parameters

budget_constraint (float) – \(r_j\), i.e. the \(j\)th \(1 \times 1\)

budget_constraints’s element.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.

- Example

Let’s directly deal with the \(\rho_j=0 \iff \sigma_j=1\) CES’s limiting case, which makes it boil down down to a Cobb-Douglas function.

>>> budc = 200. >>> ivals = np.array([[110., 90.]]) >>> iprcs = np.array([[.9, 1.1]])

>>> imsks = np.array([[1., 0.]]) >>> m = MarshallianGFCES(sigma=1, negated_mask=False) >>> m.compute_calibrand_0( ... budget_constraint=budc, input_values=ivals, ... input_volumes_drates2=imsks ... ) >>> m.calibrand_0 array([[1., 0.]]) >>> m.input_volumes_computer( ... budget_constraint=budc, input_prices=np.ones_like(ivals), ... input_values=ivals, ... ) array([[110., 90.]]) >>> m.input_volumes_computer( ... budget_constraint=budc, input_prices=iprcs, ... input_values=ivals, ... ) array([[122.22, 81.82]])

>>> imsks = np.array([[0., 1.]]) >>> m = MarshallianGFCES(sigma=1, negated_mask=True) >>> m.compute_calibrand_0( ... budget_constraint=budc, input_values=ivals, ... input_volumes_drates2=imsks ... ) >>> m.calibrand_0 array([[1., 0.]]) >>> m.input_volumes_computer( ... budget_constraint=budc, input_prices=np.ones_like(ivals), ... input_values=ivals, ... ) array([[110., 90.]]) >>> m.input_volumes_computer( ... budget_constraint=budc, input_prices=iprcs, ... input_values=ivals, ... ) array([[122.22, 81.82]])

See also

-

spendings_rooter(self, *, budget_constraint: float, input_values: np.ndarray)¶ s/e., \(1 \times 1\) unit-dimensionless zero.

(201)¶\[\approx 0\]- Parameters

budget_constraint (float) – \(r_j\), i.e. the \(j\)th \(1 \times 1\)

budget_constraints’s element.input_values (numpy.ndarray) – \((\bmcV_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_values’s slice.

-

class

iamax.library.MarshallianLeo¶

Particularized version of

MarshallianCESat \(\sigma=0\).Warning

This class has vocation to be removed sooner or later and obtained directly through the parametrization of

MarshallianCES.-

compute_calibrand_0(self, *, input_prices: np.ndarray, input_volumes: np.ndarray)¶ s/e.

(202)¶\[a_k = q_k / \sum_{k^{'} \in \mcI_j} q_{k^{'}} \ \forall k \ \in \mcI_j\]where \(q_k\) is the utility maximizing level of consumption.

- Parameters

input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.input_volumes (numpy.ndarray) – \((\bQ_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_volumes’s slice.

- Example

>>> m = MarshallianLeo() >>> _ = m.compute_calibrand_0( ... input_prices=np.ones((1, 2)), ... input_volumes=np.array([[110., 90.]]) ... ) >>> m.calibrand_0 array([[0.55, 0.45]])

-

input_volumes_computer(self, *, budget_constraint: float, input_prices: np.ndarray, **_: np.ndarray)¶ Input demands, \(1 \times |\mcI_j|\), denoted as

(203)¶\[q_k = a_k \frac{r_j}{ \sum_{k^{'} \in \mcI_j} \tbp_{k^{'}} a_{k^{'}} } \ \forall k \ \in \mcI_j\]where \(r_j\) is the budget constraint to be saturated, \(a_k\) is as in Eq.202 and \(\tbp_k\) is the \(k\)th price of consumption.

- Parameters

budget_constraint (float) – \(r_j\), i.e. a \(j\)-related \(1 \times 1\)

budget_constraints’s element.input_prices (numpy.ndarray) – \((\tbP_{k,j})_{k \in \mcI_j}\), i.e. the \(j\)th \(1 \times |\mcI_j|\)

input_prices’s slice.

- Example

>>> m = MarshallianLeo() >>> _ = m.compute_calibrand_0( ... input_prices=np.array([[1.01, .99]]), ... input_volumes=np.array([[110., 90.]]) ... ) >>> m.calibrand_0 array([[0.55, 0.45]]) >>> m.input_volumes_computer( ... budget_constraint=200, input_prices=np.ones((1, 2)), ... ) array([[110., 90.]])

-

-

class

iamax.library.EmplBMagnitude¶ Static class that aggregates a bunch of private methods related to employment- and utilization-based magnitudes.

See also

-

static

_drate_pow_increaser(*, dr: float, c: float = 1.0, s: float = 1.0)¶ Rate differential increasing function.

(204)¶\[\mfr(dr, c, s) := s\left(1 + dr\right)^{c}\]Cf. parameters section below.

- Parameters

Note

For \(c < 0\), the function turns \(dr\)-decreasing.

- Example

>>> invariants = {'c': .2, 's': 1.} >>> EmplBMagnitude._drate_pow_increaser(dr=-.5, **invariants) 0.8705505632961241 >>> EmplBMagnitude._drate_pow_increaser(dr=.0, **invariants) 1.0 >>> EmplBMagnitude._drate_pow_increaser(dr=.5, **invariants) 1.0844717711976986

-

static

_factor_pow_increaser(*, f: float, c: float = 1.0, s: float = 1.0)¶ Factor increasing function.

(205)¶\[\mfr(f, c, s) := s f^c\]- Parameters

Note

For \(c < 0\), the function turns \(f\)-decreasing.

- Example

>>> invariants = { ... 'c': .2, ... 's': 1., ... } >>> EmplBMagnitude._factor_pow_increaser(f=.5, **invariants) 0.8705505632961241 >>> EmplBMagnitude._factor_pow_increaser(f=1.0, **invariants) 1.0 >>> EmplBMagnitude._factor_pow_increaser(f=1.5, **invariants) 1.0844717711976986 >>> EmplBMagnitude._factor_pow_increaser(f=-.5, **invariants) 0.7042902001692477

-

static

_rate_tanh_increaser(*, r: float, a: float = 1.0, b: float = 1.0, c: float = 1.0, s: float = 1.0)¶ Rate increasing function.

(206)¶\[\mfr(r, a, b, c, s) := s\left( a + b \tanh(-c r) \right)\]Cf. parameters section below.

- Parameters

Note

For \(c < 0\), the order of \(a\) and \(b\) is reversed, i.e. the function turns \(r\)-decreasing.

- Example

>>> invariants = { ... 'a': .05, ... 'b': .711594155955765, ... 'c': 1.09045112440194, ... 's': 1. ... } >>> EmplBMagnitude._rate_tanh_increaser(r=.0, **invariants) 0.05 >>> EmplBMagnitude._rate_tanh_increaser(r=.5, **invariants) -0.3036148489085014 >>> EmplBMagnitude._rate_tanh_increaser(r=1., **invariants) -0.5171709549513277

-

static

-

class

iamax.library.PowCurvedNetPrice(sigma: float|np.ndarray, urate_bias: float|np.ndarray = 0.0)¶

Net-price curve abstraction, whose name stems from the generalization of the well vertued negative relationship between wages and local unemployment, a.k.a. the wage curve.

- Parameters

Note

Such elasticity is assumed to measure the sensitivity of prices to changes in market conditions relative to a specific baseline, rather than simply the level of unemployment.

-

compute_calibrand_0(self, *, output_price: np.float|np.ndarray, unemployment_rate: np.float|np.ndarray)¶ Curve parametrization, performed such that

(207)¶\[\begin{split}\up^{*}_j &= \up_{j,t=0} \\ \tau_{\neg\hq, j}^{*} &= \tau_{\neg\hq, j,t=0}\end{split}\]where \(\up_{j,t=0}\) is the (producer net) price at \(t=0\) and \(\tau_{\neg\hq, j,t=0}\) the rate of unemployed capacity at \(t=0\).

- Parameters

output_price (float) – \(\up_j\), i.e. the \(j\)th \(1 \times 1\)

output_prices’s element.unemployment_rate (float) – \(\tau_{\neg\hq, j}\), i.e. the \(j\)th \(1 \times 1\)

unemployment_rates’s element.

- Example

>>> cnp = PowCurvedNetPrice(sigma=None) >>> cnp.compute_calibrand_0( ... output_price=1e2, unemployment_rate=.1 ... ) >>> cnp.price_ref 100.0 >>> cnp.price_ref_star 100.0 >>> cnp.urate_ref 0.1 >>> cnp.urate_bias 0.0

-

compute_calibrand_0_star(self, *, deflators_fisher_drates: np.ndarray)¶ - Parameters

deflators_fisher_drates (numpy.ndarray) – \((\bmfp^{\text{drate}}_{\text{F}, k})_{k \in \mcI_j}\), i.e. a \(j\)th \(1 \times 2\) slice of

deflators_fisher_drates, whose second component is of interest.

-

output_price_computer(self, *, unemployment_rate: float, deflators_fisher: np.ndarray, output_price_drate: np.ndarray = 0.0, output_price_drate2: np.ndarray = 0.0)¶ s/e., \(1 \times 1\), denoted as